HSA vs. FSA for Mental Health Expenses: Maximizing Tax-Advantaged Benefits

If you pay for therapy with after-tax dollars while a health savings account or flexible spending account sits in your benefits package unused or underused you pay more for mental health care than you need to. The IRS allows both account types to cover a broad range of mental health expenses, yet many people in ongoing therapy either don’t know this or aren’t sure which expenses qualify, which don’t, and how to navigate the rules without running into compliance problems.

A health savings account (HSA) or flexible spending account (FSA) lets you pay for qualifying mental health care therapy, psychiatric appointments, prescriptions, and more with pre-tax dollars, meaningfully reducing what you actually spend on mental health treatment.

This article explains exactly what qualifies, what doesn’t, where the genuine gray areas exist, and how to make informed decisions about using these tax-advantaged accounts to reduce the real cost of mental health care.

Tax-advantaged accounts for healthcare sit at an intersection that most wellness publications avoid: financial planning and mental health access. We cover it because the gap between what these accounts allow and what people actually use them for is large enough to meaningfully affect whether someone can afford ongoing therapy. The rules are genuinely navigable once they are clearly explained, and that is what this article sets out to do.

Important Notice: This article provides general educational information about HSA and FSA rules for mental health expenses based on IRS guidelines. It is not tax advice and does not constitute legal or financial planning guidance. IRS rules are complex, subject to annual change, and interact with your specific plan terms, income, and individual circumstances. Consult a qualified tax professional, benefits administrator, or financial advisor for guidance specific to your situation.

Why This Matters: Mental Health as Legitimate Healthcare Expense

How Do HSA and FSA Accounts Reduce Mental Health Costs?

Paying for therapy through your HSA or FSA means every qualifying mental health dollar goes further. Because contributions enter these accounts before federal income tax applies, you spend pre-tax dollars on therapy, psychiatric care, and prescriptions rather than after-tax dollars that cost you more in real terms.

For therapy, psychiatric care, prescription mental health medications, inpatient treatment, and other qualifying expenses, this represents a meaningful cost reduction that many people never access simply because they don’t know the rules.

The Mental Health Parity and Addiction Equity Act requires insurers to cover mental health benefits no more restrictively than physical health benefits which directly affects how your mental health expenses interact with your deductible and out-of-pocket maximum, and therefore how you plan your HSA or FSA contributions.

The Tax Math: What Pre-Tax Dollars Actually Save

Your actual savings depend on your marginal federal income tax rate. A simplified illustration:

If you’re in the 22% federal marginal tax bracket:

- $150 therapy session paid out of pocket: costs $150

- $150 therapy session paid through your HSA or FSA: effective cost approximately $117 you avoided $33 in federal income tax

- Annual savings on weekly therapy: approximately $1,716 in federal tax alone

If you’re in the 24% federal marginal tax bracket:

- Same $150 session: effective cost approximately $114

- Annual savings on weekly therapy: approximately $1,872

State income tax savings add to this depending on where you live. FSA contributions through payroll deduction also skip FICA taxes 7.65% adding further benefit.

Important: These illustrations show examples based on marginal tax rates only. Your actual tax savings depend on your full tax situation, filing status, state, and other factors. Consult a tax professional for calculations specific to your circumstances.

Why Many People Don’t Realize Mental Health Qualifies

Most benefits materials never clearly communicate that mental health care qualifies as a legitimate medical expense under IRS rules. Several factors drive underutilization:

- Benefits communications emphasize physical health expenses prescriptions, dental, vision

- Mental health stigma leads people to think of therapy as optional rather than medical

- Confusion about what constitutes medical care versus general wellness

- Uncertainty about telehealth and newer service formats

- Assumption that only clearly physical conditions qualify

The IRS definition of qualified medical expenses found in IRS Publication 502 covers a broader range than many people realize, and it explicitly includes mental health treatment.

How This Changes the Real Cost of Therapy

Understanding what your HSA covers for mental health changes the economic calculation entirely. A therapist charging $175 per session who isn’t in your insurance network may become genuinely affordable when you account for:

- Payment with pre-tax dollars from your health savings account

- The absence of a deductible that must be met before insurance coverage applies

- The flexibility of out-of-network reimbursement for quality provider selection

Conversely, an in-network therapist with a $30 copay paid with after-tax dollars may cost more in effective dollars than an out-of-network therapist you pay through your HSA depending on your tax bracket and insurance structure.

HSA Basics: What You Need to Know

What Is an HSA and Who Can Have One

A Health Savings Account is a tax-advantaged savings account available to individuals who enroll in a qualified High-Deductible Health Plan (HDHP). You own the account not your employer meaning it travels with you if you change jobs or retire.

Health savings accounts deliver three tax advantages: your contributions reduce your federal income tax (or skip it entirely through payroll deduction), your funds grow tax-free, and you withdraw funds for qualifying medical expenses completely tax-free. This triple tax advantage makes the HSA among the most tax-efficient vehicles available for mental health care and all qualifying healthcare costs. Understanding your employee mental health benefits and EAP options alongside your HSA gives you a complete picture of what your employer offers for mental health support.

HDHP Requirement: The Key Eligibility Gate

To contribute to a health savings account, you must enroll in an IRS-qualified HDHP. For 2026, IRS-qualifying HDHP thresholds are:

Minimum deductible:

- Self-only coverage: $1,650

- Family coverage: $3,300

Maximum out-of-pocket limits:

- Self-only coverage: $8,300

- Family coverage: $16,600

What does HDHP mental health coverage actually mean for your out-of-pocket costs? Under an HDHP, you pay the full cost of mental health visits including therapy and psychiatric appointments until you meet your deductible. After that, your insurance covers a share. Your health savings account covers those pre-deductible costs with pre-tax dollars, which significantly reduces the real burden.

Verify current year thresholds directly with the IRS at irs.gov these figures update annually and you should confirm the 2026 figures against current IRS guidance at the time of your decision.

Additional eligibility requirements: Medicare enrollment disqualifies you from contributing. Another person cannot claim you as a dependent on their return. You cannot carry other disqualifying health coverage with specific exceptions including dental, vision, disability, and certain limited coverage.

Annual Contribution Limits (2026)

For 2026, IRS contribution limits are:

- Self-only coverage: $4,300

- Family coverage: $8,550

- Age 55+ catch-up contribution: Additional $1,000

Always verify current limits at IRS.gov before you make contribution decisions. The IRS updates limits annually through Revenue Procedure announcements.

You, your employer, or both can make contributions but total contributions from all sources cannot exceed the annual limit. Employer contributions count toward your limit.

What Is the Triple Tax Advantage of an HSA?

The health savings account’s tax benefits operate at three levels and no other account type delivers all three simultaneously:

1. Contributions: Your contributions reduce your federal income tax. Payroll deductions also skip FICA taxes Social Security and Medicare, 7.65% combined.

2. Growth: Interest, dividends, and investment gains your account earns accumulate free of federal income tax.

3. Tax-free withdrawals: You withdraw funds for qualifying medical expenses completely tax-free at the federal level meaning every dollar you pull out for qualifying mental health care costs you nothing in additional tax.

For long-term mental health care costs, the combination carries particular power. No other savings vehicle delivers this level of tax efficiency for healthcare spending.

HSA Portability and Long-Term Accumulation

You own your health savings account outright it travels with you regardless of your employment status. If you change jobs, retire, or leave your employer’s health plan, your balance goes with you.

Unlike flexible spending accounts, your HSA funds never expire. Accumulated balances roll over indefinitely from year to year. This lets the account function as a long-term mental health savings vehicle:

- Contribute during working years when you carry HDHP-eligible coverage

- Accumulate unused funds tax-free

- Draw on funds for qualifying mental health expenses at any time

- After age 65, withdraw for any purpose non-medical withdrawals generate taxable income like a traditional IRA, but you face no penalty

What Happens to Unused HSA Funds

Your unused funds roll over completely from year to year. No use-it-or-lose-it rule applies to health savings accounts. This makes them appropriate for:

- Ongoing mental health expenses you pay each year

- Future anticipated mental health expenses

- Long-term accumulation for retirement healthcare costs

If you don’t currently use your full balance for mental health care, you can invest it in mutual funds or other investments depending on your custodian’s options and minimum balance requirements and let it grow tax-free.

FSA Basics: What You Need to Know

What Is an FSA and Who Can Have One

A Flexible Spending Account is an employer-sponsored benefit account that lets you set aside pre-tax dollars for qualified medical expenses. Unlike health savings accounts, flexible spending accounts work with any health plan type not just HDHPs.

Your employer administers the FSA through a third-party administrator. You must elect your contribution amount at the start of the plan year typically during open enrollment and you generally cannot change your election mid-year without a qualifying life event.

Employer Sponsorship Requirement

Employer sponsorship is the only path to a flexible spending account. Self-employed individuals cannot open FSAs. If your employer doesn’t offer one, you have no access unlike health savings accounts, which you can open independently as long as you carry HDHP coverage.

You can hold both account types simultaneously only in limited circumstances:

- Limited Purpose FSA: Covers only dental and vision expenses while you make full HSA contributions

- Post-Deductible FSA: Becomes available for general medical expenses only after you meet the HSA-qualifying deductible

Holding a general purpose FSA while also holding a health savings account disqualifies you from making HSA contributions. Consult your plan administrator and tax advisor if you find yourself in this situation.

Annual Contribution Limits (2026)

For 2026, the FSA contribution limit is:

- Maximum employee contribution: $3,300 per year

Verify current limits at IRS.gov the IRS updates limits annually.

Employer contributions can supplement your employee contributions. Total combined contributions cannot exceed the annual IRS limit plus any employer contribution.

What Happens to Your FSA Funds If You Don’t Use Them?

Flexible spending accounts operate under a fundamental use-it-or-lose-it rule: you forfeit funds you don’t use by the plan year deadline. This is a significant limitation compared to health savings accounts and requires thoughtful election planning.

Employers can optionally offer one of two modifications:

Grace period: You get up to 2.5 months after plan year end to spend remaining funds running until approximately March 15 for calendar-year plans.

Carryover provision: You can carry over up to $660 (for 2026 verify current limit) to the next plan year.

Important: Your employer can offer only ONE of these options, not both and your employer can offer neither. Verify which option your employer’s plan offers before you make your election decision.

For predictable, ongoing mental health expenses weekly therapy sessions, for example FSA election planning is relatively straightforward. For variable or uncertain mental health expenses, the use-it-or-lose-it risk requires careful consideration.

FSA Upfront Availability

The flexible spending account delivers a significant planning advantage: your full annual election becomes available from day one of the plan year, even before you complete all your payroll contributions.

This means if you elect $3,300 for the year and your plan runs January through December, you can access all $3,300 in January even though your payroll deductions continue through December. For someone starting an intensive therapy program or inpatient treatment early in the year, this upfront availability delivers meaningful practical benefit.

Mental Health Expenses That Qualify

IRS Publication 502 defines qualified medical expenses as amounts you pay “for the diagnosis, cure, mitigation, treatment, or prevention of disease, or for the purpose of affecting any structure or function of the body.” The IRS classifies mental health conditions as diseases and medical conditions under this definition.

The following mental health expenses clearly qualify for reimbursement through your health savings account or flexible spending account:

- Individual therapy and psychotherapy in-person and telehealth

- Psychiatric appointments and medication management

- Prescription medications for mental health conditions

- Inpatient mental health treatment

- Intensive Outpatient Programs (IOP)

- Substance use disorder treatment

- Psychological testing and assessment

What Makes a Mental Health Expense HSA or FSA Eligible?

The consistent eligibility factor across all qualifying mental health expenses is the medical care purpose. A qualifying expense must serve the diagnosis, cure, mitigation, treatment, or prevention of a disease or medical condition and a licensed professional must deliver or prescribe it.

This distinguishes:

- Therapy for diagnosed depression (qualifying medical care) from life coaching for general fulfillment (not qualifying)

- Prescription antidepressants (qualifying) from OTC supplements marketed for mood (generally not qualifying)

- Psychiatric evaluation (qualifying medical care) from executive performance coaching (not qualifying)

The presence of a diagnosed mental health condition and a treatment or diagnostic purpose determines reimbursement eligibility. Every expense below qualifies because it meets this standard.

Therapy and Psychotherapy (In-Person and Telehealth)

Individual psychotherapy and counseling sessions with licensed mental health professionals licensed psychologists (PhD/PsyD), licensed professional counselors (LPC), licensed clinical social workers (LCSW), licensed marriage and family therapists (LMFT) qualify as medical expenses under IRS Publication 502 when the provider treats a mental health condition.

In-person therapy: Clearly qualifies when the provider treats a mental health condition.

Telehealth therapy: Current IRS guidance allows telehealth therapy to qualify, though telehealth rules have changed multiple times since 2020. Verify current eligibility with your plan administrator for the current tax year.

Key requirement: The therapy must treat a diagnosed medical condition not general personal development, wellness, or life coaching.

Psychiatric Appointments and Medication Management

Can you use your FSA for a psychiatrist? Yes. Appointments with licensed psychiatrists (MD or DO) for evaluation, diagnosis, and medication management qualify as medical expenses. This includes:

- Initial psychiatric evaluations

- Follow-up medication management appointments

- Telehealth psychiatric appointments

- Crisis psychiatric evaluation

Psychiatric services rank among the clearest qualifying expenses because licensed medical physicians perform the diagnosis and treatment.

Prescription Medications for Mental Health Conditions

Prescription medications for mental health conditions antidepressants, anti-anxiety medications, mood stabilizers, antipsychotics, medications for ADHD, and others qualify for reimbursement through both account types.

This includes medications you obtain at pharmacies, mail-order prescriptions, and generic and brand-name prescription medications. A licensed prescriber must write a valid prescription. Over-the-counter supplements or products marketed for mental wellness generally do not qualify unless a provider specifically prescribes them for a medical condition verify with your plan administrator.

Inpatient Mental Health Treatment

Inpatient mental health treatment at licensed psychiatric facilities or mental health units of hospitals qualifies as a medical expense. This includes:

- Acute inpatient psychiatric hospitalization

- Residential mental health treatment

- Medically necessary inpatient stays for eating disorders, severe depression, bipolar disorder, and similar conditions

Your account covers treatment facility fees, therapy and psychiatric services the facility provides, and related medical costs.

Intensive Outpatient Programs (IOP)

Intensive Outpatient Programs structured mental health treatment programs typically involving multiple hours of treatment several days per week generally qualify as medical expenses when treating a diagnosed mental health condition. Verify specific program eligibility with your plan administrator, as IOP structures vary and documentation requirements may apply.

Substance Use Disorder Treatment

Substance use disorder treatment qualifies as a medical expense under IRS Publication 502, which explicitly classifies treatment for alcohol and drug addiction as qualified medical expenses. This includes inpatient substance use disorder treatment, outpatient treatment programs, medically supervised detoxification, and therapy for substance use disorders.

Psychological Testing and Assessment

Psychological testing and assessment including neuropsychological evaluation, psychological evaluation for diagnosis, ADHD assessment, and similar professionally administered assessments qualifies as medical care when licensed psychologists or other qualified professionals conduct them for diagnostic purposes.

Mental Health Expenses That Do NOT Qualify

Not every mental wellness expense qualifies for reimbursement through your health savings account or flexible spending account. The following expenses generally do not qualify:

- General wellness programs and apps without medical diagnosis

- Life coaching not the same as licensed therapy

- Meditation apps and stress reduction programs for general wellness

- Marriage and couples counseling complex eligibility rules (see Gray Areas)

- Career counseling and personal development

General Wellness Programs and Apps (Without Medical Diagnosis)

General wellness programs, stress reduction programs, and wellness apps that marketers target to the general public for stress, happiness, or mental wellness without treating a specific diagnosed medical condition generally do not qualify as medical expenses.

The IRS does not allow deductions for wellness products and programs that are merely beneficial to general health under IRS Publication 502. Do over-the-counter mental health supplements qualify? Generally no unless a licensed provider specifically prescribes them for a diagnosed medical condition, OTC supplements and wellness products fail the medical care test.

Life Coaching (Not the Same as Therapy)

Life coaching personal development, goal-setting, performance enhancement, career guidance that non-licensed coaches deliver generally does not qualify as a medical expense regardless of how beneficial it may be. The IRS applies consistent logic here: treatment of a medical condition by a qualified professional qualifies; personal development and performance coaching generally does not. Executive therapy programs delivered by licensed therapists are a different matter these may qualify when treating a diagnosed condition.

Meditation Apps and Stress Reduction Programs (Generally)

IRS rules generally exclude meditation apps including well-known applications like Calm and Headspace when you purchase them for general wellness stress reduction programs, and relaxation tools that marketers target to the general public from qualifying expenses.

Exception consideration: If a licensed physician prescribes a specific app or program as treatment for a diagnosed medical condition and provides a letter of medical necessity, it may potentially qualify but this sits in a genuinely gray area requiring verification with your plan administrator and tax advisor.

Career Counseling and Personal Development

Career counseling, professional development programs, leadership training, and personal development courses do not qualify as medical expenses under IRS rules. These serve professional advancement purposes, not medical treatment.

The Medical Care Distinction That Determines Eligibility

Every ineligible expense fails the same test: it doesn’t constitute treatment, diagnosis, prevention, or mitigation of a disease. When you evaluate any borderline expense, ask: “Does this treat or diagnose a specific medical condition, and does a qualified professional deliver it?” If the primary purpose is personal improvement, relationship enhancement, or general wellness it likely doesn’t qualify.

The Gray Areas: Expenses With Complex Eligibility

Telehealth Mental Health Services: Current Rules

Current IRS guidance allows telehealth therapy to qualify as a medical expense when licensed professionals treat mental health conditions. The expense eligibility whether therapy sessions via video qualify is generally clear. Platforms like BetterHelp and Talkspace deliver licensed therapy sessions that qualify for reimbursement. Eligibility follows the nature of the service, not the platform. A detailed cost breakdown of both platforms is useful context when you are calculating the effective cost after pre-tax account reimbursement.

The more complex telehealth question involves HSA eligibility for the underlying health plan. The CARES Act (2020) and subsequent legislation created temporary provisions allowing health savings accounts to cover telehealth services before you meet the HDHP deductible without losing HSA eligibility. Congress has required periodic reauthorization of these provisions.

For current tax year rules: Verify the current status of telehealth safe harbor provisions with your plan administrator and current IRS guidance. Current IRS guidance allows telehealth therapy to qualify as a medical expense when licensed professionals treat mental health conditions. The more complex telehealth question involves HSA eligibility for the underlying health plan. For a full breakdown of how telehealth therapy works across state lines, including the licensure requirements that affect whether your provider can legally see you, the detail is here.

Does Couples Counseling Qualify for HSA or FSA?

This sits in a genuine gray area and ranks among the most frequently asked questions about using tax-advantaged accounts for mental health care.

The general IRS position: Counseling that primarily aims to improve a relationship or resolve marital difficulties does not constitute medical care under IRS Publication 502.

The exception: If a licensed therapist treats one or both partners for a diagnosed mental health condition and couples therapy forms part of that treatment the expense may qualify as medical care.

More likely to qualify:

- One or both partners carries a diagnosed mental health condition

- Couples therapy explicitly forms part of the treatment plan for that condition

- The treating therapist holds a license and can document medical necessity

- The primary purpose is treating a diagnosed condition, not general relationship improvement

Less likely to qualify:

- Neither partner carries a diagnosed mental health condition

- The primary purpose is communication improvement or relationship enrichment

- An unlicensed coach rather than a licensed therapist delivers the service

Practical guidance: Before you submit couples therapy for reimbursement, discuss documentation with your therapist and contact your plan administrator about their specific requirements. A letter of medical necessity from the treating therapist may support eligibility when a diagnosed condition is under treatment. Financial disagreements in relationships including disagreements about therapy costs often surface alongside these eligibility questions.

The couples counseling eligibility question illustrates something broader about how these accounts work in practice: the IRS framework was designed around a relatively traditional model of discrete medical treatment, and it does not map cleanly onto the way many people actually use mental health care today. Preventive therapy, maintenance therapy for people who are functioning well but want ongoing support, and integrative approaches that blend clinical treatment with personal growth work all sit in territory the IRS rules do not address with precision. This is not a reason to avoid using these accounts. It is a reason to document carefully, ask your plan administrator specific questions before spending, and consult a tax professional when the expense genuinely sits at the edge of the eligibility framework. The accounts are more useful than most people realize. They also require more deliberate navigation than the marketing around them typically suggests.

Employee Assistance Programs (EAP) and Account Interaction

Your employer funds EAP sessions as a benefit you generally don’t draw on your health savings account or flexible spending account to pay for them. Relevant intersections include:

- Transitioning from EAP to insurance-covered therapy: You can pay post-EAP therapy sessions with insurance cost-sharing from your HSA or FSA

- EAP itself doesn’t affect HSA eligibility: Having EAP access doesn’t disqualify you from making health savings account contributions

Mental Health Apps: Emerging Eligibility Landscape

The eligibility of mental health apps continues to evolve. Current general principles:

Generally not eligible: Apps that marketers target to the general public for wellness, stress reduction, mood improvement, or meditation without a specific medical purpose.

Potentially eligible: Apps that a licensed physician or therapist specifically prescribes as treatment for a diagnosed medical condition with appropriate documentation.

Prescription digital therapeutics: A category of FDA-cleared digital health products that manufacturers specifically design to treat clinical conditions. Some argue these qualify with a valid prescription. Verify with your plan administrator.

The IRS has not published comprehensive guidance on mental health app eligibility. Plan administrators interpret this area differently. When in doubt, contact your administrator before you spend.

Letter of Medical Necessity

A licensed healthcare provider writes a Letter of Medical Necessity (LOMN) to state that a specific product or service is medically necessary for the treatment of a diagnosed condition. A LOMN can potentially strengthen your eligibility claim for expenses in genuinely gray areas.

When a LOMN may help:

- The receipt alone doesn’t make the medical purpose obvious

- Your plan administrator requires additional documentation for products or services in gray areas

- The expense could reasonably fall under either medical or general wellness

What a LOMN cannot do: Make clearly ineligible expenses eligible. A letter of medical necessity doesn’t make life coaching, general wellness apps, or gym memberships qualify under IRS rules. It provides supporting documentation for genuinely gray-area expenses it doesn’t override IRS eligibility rules.

How to request one: Ask your treating physician, psychiatrist, or therapist to write a letter on their letterhead stating the diagnosed condition, the recommended treatment or product, and why it is medically necessary. Keep this documentation with your records.

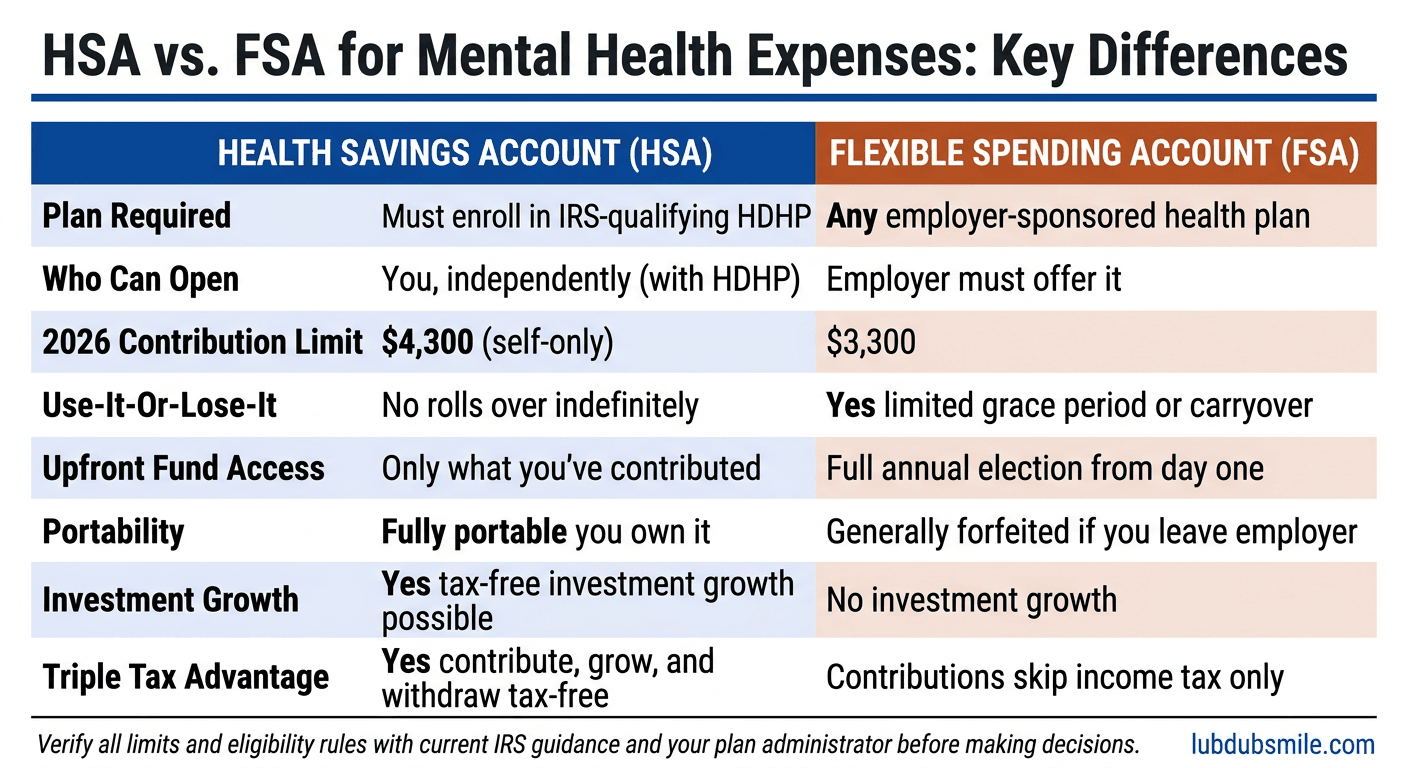

HSA vs. FSA: Which Is Better for Mental Health Expenses?

Side-by-Side Comparison

| Factor | HSA | FSA |

|---|---|---|

| Plan requirement | Must enroll in IRS-qualifying HDHP | Any employer-sponsored plan |

| Availability | You or your employer can contribute | Employer-sponsored only |

| 2026 contribution limit (individual) | $4,300 | $3,300 |

| Use-it-or-lose-it | No rolls over indefinitely | Yes with limited grace period or rollover options |

| Upfront availability | Only amount contributed to date | Full annual election available January 1 |

| Portability | Fully portable you own it | You forfeit it if you leave your employer generally |

| Investment options | Yes you can invest for tax-free growth | No funds don’t earn investment returns |

| Triple tax advantage | Yes | Contributions skip income tax; no investment growth |

| Best for ongoing expenses | Yes long-term accumulation option | Yes predictable expenses within plan year |

| Best for unexpected expenses | Less upfront availability | Full election available immediately |

Verify all limits and rules with current IRS guidance and your plan administrator.

What Is the Difference Between HSA and FSA for Mental Health?

The difference between using a health savings account versus a flexible spending account for mental health expenses comes down to four factors: eligibility, flexibility, contribution limits, and long-term value.

- Eligibility: Health savings accounts require HDHP enrollment flexible spending accounts work with any employer-sponsored plan

- Flexibility: Health savings accounts roll over indefinitely flexible spending accounts operate under use-it-or-lose-it rules

- Contribution limits: Health savings accounts allow higher contributions $4,300 vs $3,300 for 2026

- Long-term value: Health savings accounts offer investment growth and triple tax advantage flexible spending accounts offer upfront availability

For most people with ongoing therapy costs and HDHP eligibility, the health savings account delivers superior long-term value. For people without HDHP access or who need funds immediately early in the year, the flexible spending account delivers meaningful pre-tax savings with practical upfront advantages.

If You Have Predictable, Ongoing Mental Health Expenses

For individuals in ongoing weekly or bi-weekly therapy with predictable annual costs, both accounts work well your health plan eligibility primarily drives the choice. With predictable costs, FSA election is straightforward: estimate your annual therapy costs accurately, elect that amount, and capture pre-tax savings without significant forfeiture risk.

If Your Mental Health Expenses Are Variable or Unpredictable

Variable mental health expenses starting therapy mid-year, uncertain treatment intensity, or anticipating episodic rather than ongoing care create flexible spending account planning challenges because of the use-it-or-lose-it rule.

Conservative FSA strategy: Elect a lower amount you’re confident you’ll spend, avoiding forfeiture risk. You’ll miss some pre-tax savings but won’t forfeit unused funds.

Health savings account advantage: No forfeiture risk means you can contribute the maximum and draw on funds as needed without the planning anxiety that the use-it-or-lose-it rule creates.

The Long-Term Accumulation Case for Your Health Savings Account

For individuals who carry HDHP coverage, have strong finances, and don’t need to draw on their health savings account for current mental health expenses, the investment potential creates a compelling long-term strategy:

- Contribute the annual maximum

- Pay current mental health expenses out of pocket if you can afford to

- Keep receipts for all qualifying mental health expenses you pay out of pocket

- Let your account grow tax-free through investment

- Reimburse yourself later for past expenses you face no time limit on reimbursement, as long as you incurred the expense after you established the account

This strategy maximizes the triple tax advantage. It requires the financial capacity to pay current expenses out of pocket, which isn’t feasible for everyone. Consult a financial advisor before you pursue this approach.

When the FSA’s Upfront Availability Matters

The flexible spending account’s full annual election availability from day one creates specific value when:

- You start an inpatient mental health treatment program early in the year

- You face a large mental health expense early in the plan year

- You need funds before you’ve accumulated sufficient health savings account balance

If you elected $3,000 for your flexible spending account and need to pay for an intensive outpatient program in February before you’ve contributed $3,000 through payroll, the full $3,000 becomes available immediately. Your health savings account only gives you access to what you’ve actually contributed.

HDHP Trade-Off: Higher Deductible vs. Tax Benefits

Choosing an HDHP to access health savings account benefits involves a fundamental trade-off. For individuals with significant, predictable mental health expenses, compare the total annual cost of the HDHP premium multiplied by 12, plus expected out-of-pocket, plus tax savings versus a PPO or other plan higher premium multiplied by 12, plus lower deductible, plus flexible spending account tax savings. This calculation is individual-specific and worth completing with a benefits counselor during open enrollment.

Maximizing Your Tax-Advantaged Mental Health Spending

Coordinating Your Account with Your Insurance Deductible

Understanding how your deductible interacts with your health savings account or flexible spending account helps you optimize what you spend on mental health care:

For HDHP with HSA: You can pay mental health expenses from your health savings account with pre-tax dollars before you meet your deductible. Once you meet your deductible, your insurance begins covering mental health care and you can pay any remaining cost-sharing from your account.

For PPO/HMO with FSA: You can pay mental health copays and coinsurance from your flexible spending account after you meet your deductible. You can also use these funds for out-of-network mental health care your insurance doesn’t cover.

Strategy: Draw on your health savings account or flexible spending account for mental health deductible spending, copays, and out-of-pocket costs throughout the year. You pay every qualifying dollar with pre-tax money.

Can I Use My HSA for an Out-of-Network Therapist?

Yes. Eligibility for reimbursement doesn’t limit you to in-network providers. You can use your health savings account or flexible spending account for qualifying mental health expenses you pay to any licensed provider in-network or out-of-network. This is one of the most significant practical advantages of these accounts: you can select any qualified therapist based on fit and expertise, then pay with pre-tax dollars regardless of network status. For individuals seeking quality therapy outside their insurance network, comparing therapy platforms and costs helps identify the most cost-effective approach when combined with account reimbursement.

Strategic Contribution Timing for Mental Health Expenses

Flexible spending account election strategy:

- Review the prior year’s mental health expenses to estimate the current year accurately

- Include therapy sessions, psychiatric appointments, and prescription costs in your estimate

- Add any anticipated changes new treatment modality, medication changes, an anticipated intensive program

- Account for the use-it-or-lose-it risk by staying somewhat conservative if expenses are uncertain

- Verify which grace period or rollover option your employer offers this affects your forfeiture risk calculation

Health savings account contribution strategy:

- Maximize contributions when you can afford to particularly in high-income years when the tax deduction delivers the most value

- Consider front-loading contributions early in the year if you anticipate significant mental health expenses

- If you can pay current expenses out of pocket and save receipts for future reimbursement, your account investment grows tax-free in the meantime

Documenting Mental Health Expenses for Reimbursement

Proper documentation protects you in the event of an audit or plan administrator review. For mental health expenses you pay through either account, retain:

For each qualifying expense:

- Receipt or invoice showing provider name, date of service, and amount paid

- Explanation of Benefits (EOB) from insurance if you billed insurance

- Description of service therapy session, psychiatric appointment, prescription

- Provider credentials visible on documentation

Documentation retention: Keep records for the current tax year plus at least three years the general IRS audit statute of limitations. For health savings account reimbursements you take in later years for current expenses, keep documentation until you take the reimbursement plus three years.

Electronic documentation: Most plan administrators accept electronic receipts and EOBs. Scan and store physical receipts they fade over time.

Avoiding Common Compliance Mistakes

Using account funds for ineligible expenses: You pay income tax on the distribution plus a 20% penalty when you use health savings account funds for non-qualifying expenses. Know what qualifies before you spend.

FSA forfeiture: Electing too high an amount for your flexible spending account and forfeiting unused funds costs you money. Conservative election or careful planning prevents this.

Missing the FSA reimbursement deadline: Your flexible spending account plan sets reimbursement deadlines often 90 days after the plan year ends. Submit all eligible expenses before the deadline.

Inadequate documentation: Your plan administrator can deny reimbursement requests when you provide insufficient documentation. Retain receipts and EOBs for all submissions.

Double-dipping: You cannot claim a reimbursed expense as a tax deduction on your income tax return. Expenses you pay pre-tax through these accounts cannot also generate an itemized medical deduction.

Special Situations and Considerations

Can Self-Employed Individuals Access These Tax Benefits for Mental Health?

Yes through the health savings account, not the flexible spending account. Self-employed individuals can open and contribute to a health savings account as long as they carry a qualifying HDHP. Without employer sponsorship, you purchase your own HDHP through the marketplace or directly from an insurer and open your account through a bank or financial institution.

Self-employed tax treatment: You deduct health savings account contributions above the line you don’t need to itemize making them available regardless of whether you take the standard deduction.

Flexible spending account access: Self-employed individuals generally cannot establish flexible spending accounts for themselves. The health savings account is the primary tax-advantaged option available to self-employed individuals seeking to pay for mental health care with pre-tax dollars. Understanding concierge medicine vs traditional care can also help self-employed individuals evaluate their broader healthcare options alongside account planning.

COBRA and Account Continuation

Health savings account during COBRA: If you lose HDHP coverage and elect COBRA to continue it, you can continue contributing to your health savings account as long as your COBRA plan qualifies as an HDHP. Your existing balance remains available for qualifying expenses regardless.

Flexible spending account during COBRA: FSA continuation under COBRA is more complex. Some plans offer COBRA continuation; others don’t. If your plan offers it, you pay the full employee and any employer contribution plus an administrative fee. Given that funds you’ve already contributed remain available for use, COBRA continuation delivers the most value when you carry a significant positive balance at termination.

Spouse and Dependent Mental Health Expenses

You can use your health savings account or flexible spending account to cover qualifying mental health expenses for your spouse and tax dependents not just yourself. This includes:

- Therapy, psychiatric care, and prescriptions for your spouse

- Mental health treatment for dependent children

- Qualifying mental health expenses for other tax dependents

A single health savings account or family flexible spending account election can cover your family’s total mental health therapy expenses including children’s therapy, individual therapy for each spouse, and psychiatric appointments.

Medicare Enrollment and Contribution Rules

Enrolling in Medicare Part A or Part B disqualifies you from making additional health savings account contributions. This is a critical planning point for individuals approaching Medicare eligibility at age 65:

- Medicare enrollment stops your contributions

- Your existing balance continues to cover qualifying expenses

- After age 65, you can use your health savings account to pay Medicare premiums Parts B, C, and D

- After age 65, you pay income tax on non-medical withdrawals but face no penalty

If you’re approaching 65 and carry significant health savings account funds, consult a financial advisor about the optimal timing of Medicare enrollment relative to your contributions.

Open Enrollment Decision Framework for Mental Health Costs

When you choose between plans during open enrollment with significant mental health expenses:

<strong>Step 1: List your anticipated annual mental health expenses therapy sessions multiplied by frequency and cost, psychiatric appointments, prescriptions.

<strong>Step 2: Calculate the HDHP total annual cost premium multiplied by 12, plus expected out-of-pocket, plus health savings account tax savings.

<p><strong>Step 3: Calculate the PPO/HMO total annual cost premium multiplied by 12, plus expected copays and coinsurance, plus flexible spending account tax savings.

<strong>Step 4: Compare total costs across scenarios, including the long-term value of health savings account accumulation if you choose the HDHP.

<strong>Step 5: Consider your risk tolerance HDHP exposes you to higher costs if your mental health needs exceed your plan. If you need support understanding your rights before making this decision, knowing when to seek professional support for anxiety can help you estimate your likely mental health utilization more accurately.

Documentation and Compliance

What Records to Keep for Mental Health Expenses

For each qualifying mental health expense you pay through either account, retain:

Provider documentation:

- Provider name and credentials

- Date of service

- Type of service individual therapy session, psychiatric appointment, etc.

- Amount the provider charged and amount you paid

Payment documentation:

- Receipt, invoice, or credit card statement

- Debit card transaction record from your account

- Explanation of Benefits from insurance when applicable

Prescription documentation:

- Pharmacy receipt showing prescription name, date, and amount

- Prescription label you can retain this digitally

Letters of medical necessity when applicable:

- Keep the original letter with provider signature

- Note the expense it covers

How Reimbursement Works (Process and Timeline)

Health savings account reimbursement:

- Pay the qualifying mental health expense using your account debit card, or pay out of pocket and request reimbursement

- If you pay out of pocket: log in to your account and submit a reimbursement request with documentation

- Many administrators process reimbursements within 3–5 business days

- You face no deadline for reimbursing yourself for past expenses, as long as you incurred the expense after you established the account

Flexible spending account reimbursement:

- Pay the qualifying expense using your FSA debit card, or pay out of pocket and submit for reimbursement

- FSA debit card transactions may require substantiation retain your receipts

- Submit out-of-pocket reimbursement requests through your administrator’s portal with documentation

- Submit all claims before your plan’s reimbursement deadline typically 90 days after plan year end

What to Do If a Claim Is Denied

If your plan administrator denies a mental health expense reimbursement:

- Request a written explanation ask for the specific reason for the denial

- Review the reason did you provide insufficient documentation, or does the plan consider this expense ineligible?

- Gather additional documentation if the denial stems from insufficient documentation, provide the missing information

- Request reconsideration most administrators run an appeals or reconsideration process

- Consider a letter of medical necessity if the expense sits in a gray area, a LOMN from your provider may support reconsideration

- Consult a tax professional if the eligibility question is genuinely complex, professional guidance may be warranted

Don’t assume a denial means the expense is definitively ineligible administrative errors and documentation issues cause many denials that you can reverse.

IRS Audit Risk and Documentation

When you use health savings account funds for non-qualifying expenses, you face significant tax risk: income tax on the amount plus a 20% penalty. In an audit, you may need to demonstrate that your distributions covered qualifying medical expenses.

Maintain complete documentation for all distributions not just mental health expenses. The IRS doesn’t require you to submit documentation when you take distributions but you must produce it if they audit you. For mental health expenses specifically, documentation of the medical condition and qualifying treatment purpose strengthens your position if anyone questions it.

Frequently Asked Questions

What Is the Difference Between HSA and FSA for Mental Health Expenses?

The difference comes down to eligibility, flexibility, and long-term value. Health savings accounts require HDHP enrollment and deliver a triple tax advantage contributions reduce your tax, funds grow tax-free, and you withdraw tax-free for qualifying expenses. Flexible spending accounts work with any employer-sponsored plan but operate under use-it-or-lose-it rules. Health savings accounts roll over indefinitely and allow investment growth. Flexible spending accounts make your full annual election available immediately. For most people with ongoing therapy costs and HDHP eligibility, the health savings account delivers superior long-term value.

Can I Use My HSA or FSA for Therapy Sessions?

Yes, generally. Individual therapy sessions with a licensed mental health professional licensed psychologist, LCSW, LPC, LMFT, or psychiatrist treating a mental health condition qualify as medical expenses under IRS Publication 502. This applies to both in-person and telehealth sessions. Verify current telehealth rules with your plan administrator. General wellness coaching or life coaching does not qualify for reimbursement through either account.

Does Couples Counseling Qualify for HSA or FSA?

This sits in a genuine gray area. Couples counseling that primarily aims to improve a relationship generally does not qualify as medical care under IRS rules. However, if couples therapy treats a diagnosed mental health condition in one or both partners, it may qualify. Before you submit couples therapy for reimbursement, discuss documentation with your therapist and contact your plan administrator. A letter of medical necessity may support reimbursement when a diagnosed condition is under treatment.

Can I Use My Account for Mental Health Apps Like BetterHelp or Talkspace?

It depends on what you’re paying for. Therapy sessions that licensed therapists conduct via telehealth platforms generally qualify for reimbursement eligibility follows the nature of the service, not the platform. Subscription fees for apps that bundle therapy with general wellness features sit in more complex territory. Contact your plan administrator with specific fee documentation to determine whether the therapy component qualifies.

What Happens If I Use My HSA for Ineligible Expenses?

The consequences are significant. When you use health savings account funds for a non-qualifying expense and you’re under age 65, the IRS includes the amount in your gross income for federal tax purposes and you pay a 20% excise tax penalty on top of the income tax. If you catch the mistake, you may correct it by returning the funds to your account by your tax filing deadline. Contact your administrator promptly. After age 65, non-qualifying withdrawals generate taxable income but you face no penalty.

Can I Reimburse Myself for Past Mental Health Expenses?

Yes with an important condition. You can reimburse yourself from your health savings account for qualifying expenses you incurred at any time after you established the account, with no deadline for taking the reimbursement. Pay mental health expenses out of pocket this year, keep your receipts, and reimburse yourself years later potentially after your funds have grown tax-free through investment. You must have incurred the expense after you established your account, and you must not have previously deducted it or received reimbursement through another source.

Professional Guidance

The Educational Purpose and Limits of This Article

This article provides general educational information about using health savings accounts and flexible spending accounts for mental health expenses, based on IRS Publication 502 and related guidance as of January 2026, provides educational information only not tax advice, legal advice, or financial planning guidance.

This article cannot account for your specific tax situation, filing status, income level, or state tax rules. It cannot address your specific employer plan’s additional restrictions or requirements, it cannot guarantee that your plan administrator will approve specific expenses and it reflects IRS rules as of January 2026 these rules change, and you should review current IRS publications annually before making decisions.

When to Consult a Tax Professional

Consult a qualified tax professional CPA, enrolled agent, or tax attorney for:

- Open enrollment decisions with significant financial impact

- Large health savings account strategy decisions maximum contributions, reimbursement timing strategy

- Determining eligibility for expenses in genuinely gray areas

- Self-employed health account planning

- Medicare transition planning relative to your health savings account

- Any situation where the tax implications are material to your financial situation

Consult your plan administrator for specific expense eligibility under your plan’s rules, documentation requirements, grace period and rollover provisions, and appeals of denied reimbursement claims.

Verifying Current IRS Rules and Contribution Limits

The IRS updates rules governing health savings accounts, flexible spending accounts, contribution limits, and qualifying expense definitions annually. Always verify current-year information before you make contribution elections or reimbursement decisions.

Official resources:

- IRS Publication 502 Medical and Dental Expenses: the IRS updates this annually primary reference for qualifying expense definitions

- IRS Publication 969 Health Savings Accounts and Other Tax-Favored Health Plans: comprehensive guidance on both account types

- IRS contribution limits: The IRS updates these annually through Revenue Procedures at irs.gov

- Healthcare.gov HDHP information: For understanding HDHP requirements for health savings account eligibility

The IRS website (irs.gov) is the authoritative source for current rules. Your plan administrator is the authoritative source for your specific plan’s requirements.

Crisis and Mental Health Access Resources

If financial barriers prevent you from accessing mental health care:

- 988 Suicide and Crisis Lifeline: Call or text 988 free, 24/7

- SAMHSA National Helpline: 1-800-662-4357 free, confidential, 24/7

- Community mental health centers: Sliding-scale fees based on income

- Federally Qualified Health Centers: findahealthcenter.hrsa.gov sliding-scale mental health services

- Open Path Collective: Reduced-rate therapy sessions ($30–$80) for those without adequate coverage

Understanding how to use your health savings account or flexible spending account for mental health care is one part of reducing financial barriers to treatment. Official resources and qualified professionals can help you navigate the full landscape of your options.

Using your HSA or FSA for mental health expenses including therapy, psychiatric care, and prescriptions reduces what you actually pay for mental health treatment by covering qualifying costs with pre-tax dollars.

This article provides general educational information about HSA and FSA rules for mental health expenses based on IRS guidelines as of January 2026. It is not tax advice and does not constitute legal or financial planning guidance. IRS rules are complex, subject to annual change, and interact with your specific plan terms, income, and individual circumstances. Consult a qualified tax professional, benefits administrator, or financial advisor for guidance specific to your situation.

This content is for educational purposes and does not substitute for professional psychological or therapeutic help.